Efforts to manage carbon footprint have been here for some decades, mostly thanks to voluntary pledges of individual companies and organisations. With the recent adoption of the ESG legislation, it became part of wide-ranging reporting obligations. One of the most notable cases is the EU CSRD. It sets the reporting obligations for the companies towards their stakeholders. That includes their approach to all relevant non-financial risks management, their efforts not to create burdens and preparedness to face the challenges.

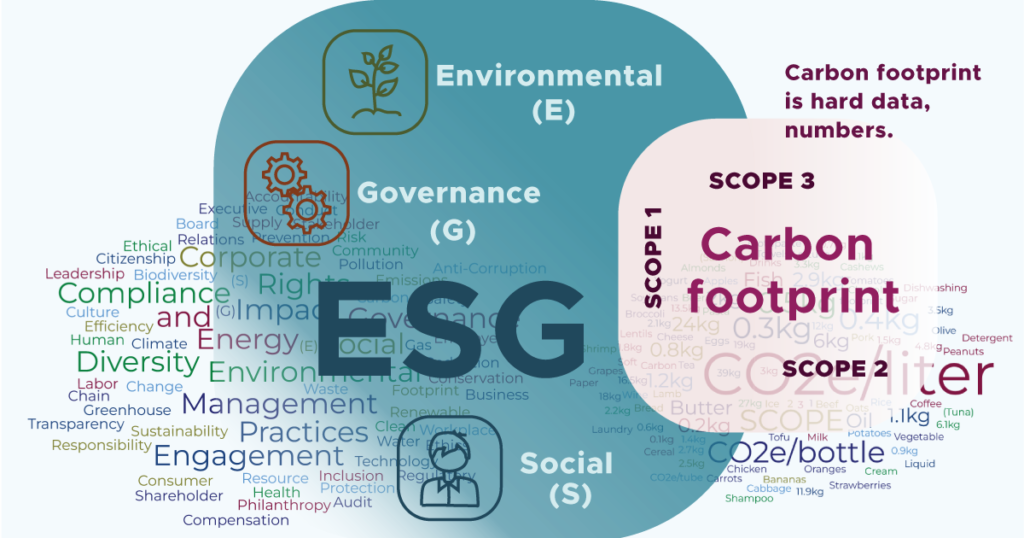

Calculating GHG emissions became part of this exercise. Sure, they cause substantial negative environmental impacts, hence their prominent position in the “E” component. However, when it comes to their reporting and management, there are also notable differences between the carbon footprint and other issues covered by the broad ESG umbrella:

Quantitative nature

The very problem with the GHG emissions is their quantity. On top of it come interpretations, methodologies, reports. That is much different than many other aspects, especially in the “S” and “G” domains. There, the nature of the problem is very often qualitative. Various quantifications are then mere attempts to represent the selected aspects of the current/desired state.

Absoluteness

Given the nature of the climate change, there is nothing relative about GHG emissions once different gases are converted to CO2 equivalents. It doesn’t matter if 1 ton of CO2e is emitted by a plane flying over Europe, coal-fired power plant in Asia or decomposing wood in America.

Supply chain view

Partially thanks to the previous features, carbon footprint can – and should be – calculated as a sum of contributions of all relevant activities leading to the realization of a given product. Carbon reports users rightly expect that the calculation will break out from the boundaries of an organisation. Only a holistic supply chain view approximates the real picture.

Reflecting on these aspects, the bottom line is the following: Carbon footprint is hard data, numbers. That reduces the possibility to shrug off the reporting requirements by means of text-generative artificial or natural intelligence. On the other hand, it provides space for automated processes based on clear logic, and not starting from the scratch after every reporting period. Carbon footprint is in this respect much closer to the financial data than to the non-financial characteristics. And you would not process your invoices and bank statements with Word and Excel, would you?